Unpromptd Team

Dec 18, 2025

The Paradox: Southeast Asia's programmatic advertising market is experiencing unprecedented cost inflation not because it's mature, but because it's chaotic. CPM inflation is outpacing wage growth across every major SEA country, programmatic auction competition is intensifying, and TikTok's dominance is reshaping the entire regional cost structure. This cost explosion reveals a counterintuitive truth: rising advertising costs signal undersaturation and supply fragmentation, not market maturity.

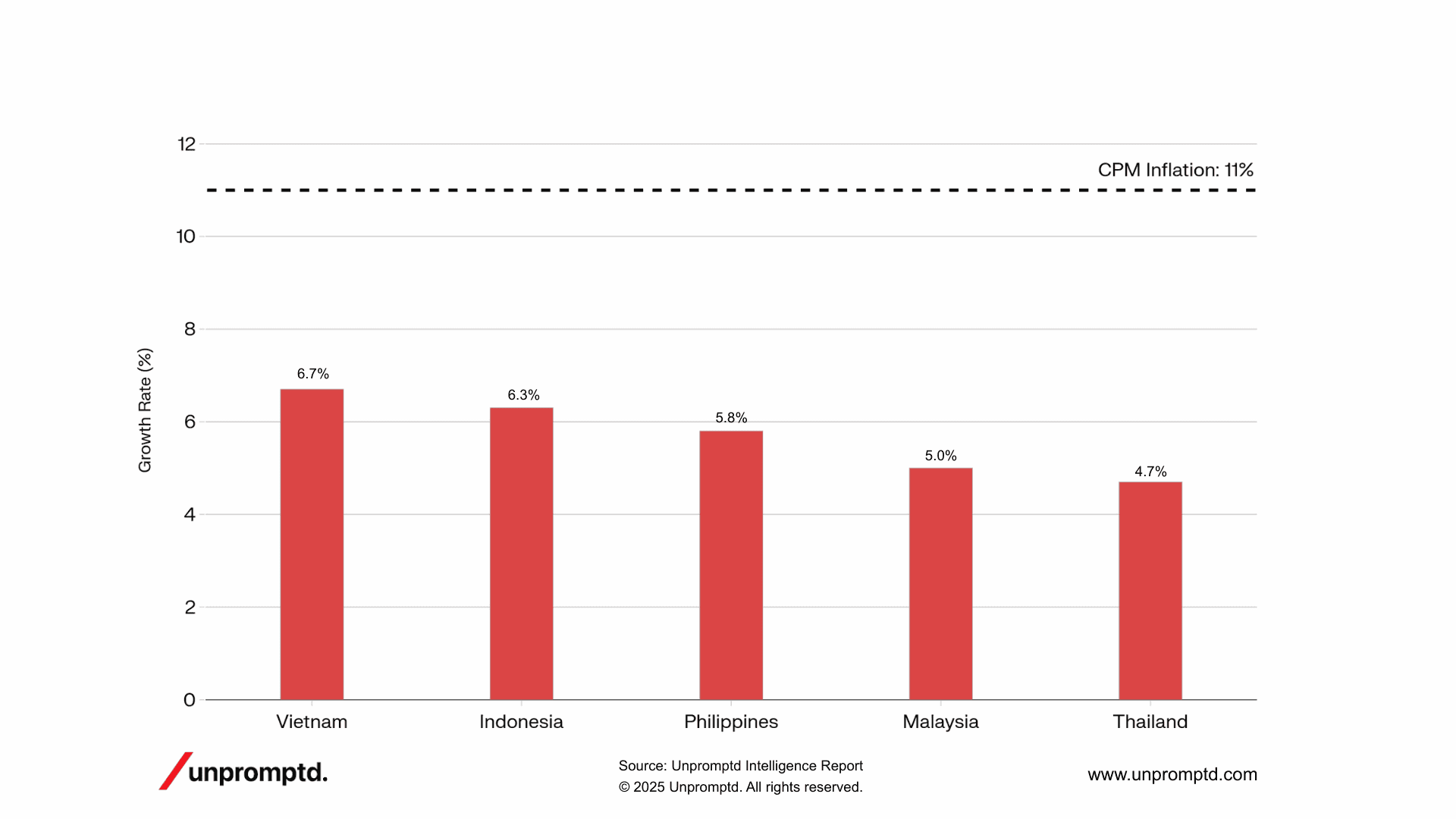

CPM Inflation vs. Wage Growth in Southeast Asia (2024-2025)

The CPM Inflation Reality: Rising Faster Than Consumer Income

In 2024, programmatic video and mobile CPMs in Southeast Asia surged by an estimated 8-14% year-on-year, with ~11% representing a blended midpoint across Meta, TikTok, and open-web programmatic benchmarks. More concerning for performance marketers is the regional divergence: this inflation rate isn't uniform; it's concentrated in high-opportunity markets like Vietnam, Indonesia, and the Philippines, where competitiveness is at its peak.

Meanwhile, wage growth across the region is dramatically lower. Vietnam, the fastest-growing economy in SEA, projects wage increases of 6.7% for 2025, followed by Indonesia at 6.3%, Philippines at 5.8%, and Thailand at 4.7%. Singapore, despite being the most mature digital advertising market in the region, is seeing only 4.4% wage growth.

This creates a cost-to-income mismatch of approximately 3-6 percentage points across SEA markets. Advertisers are paying premium rates for access to consumers whose discretionary spending isn't growing at corresponding rates. For performance marketers, this means lower customer lifetime value relative to acquisition costs a fundamental erosion of unit economics. The WFA's latest Outlook report reinforces this trend, projecting media inflation in Asia-Pacific will reach 9% in India by 2025, with Southeast Asia tracking similarly. These are not gentle corrections; they're structural cost shifts that fundamentally change how brands should approach the region.

The Auction Overcrowding Effect: More Bidders, Artificially Higher CPMs

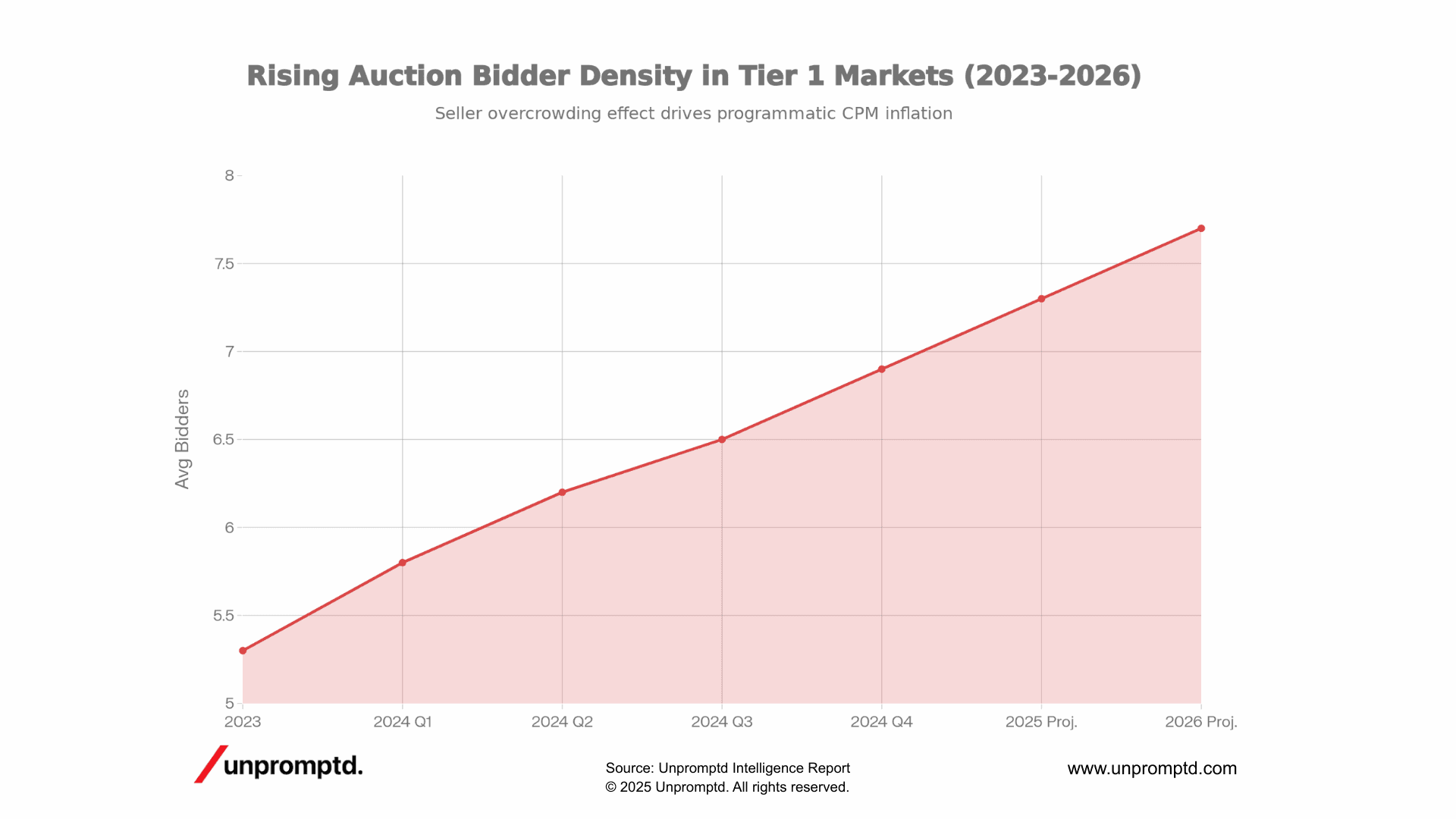

The SEA programmatic ecosystem is experiencing unprecedented seller and bidder concentration. Estimated effective auction bid depth in Tier 1 SEA markets increased from approximately 5.3 bidders per impression in 2023 to ~6.8–6.9 in 2024, representing roughly a 30% increase in competitive pressure. These figures reflect modeled auction intensity based on advertiser growth, seller density, DSP proliferation, and observed CPM inflation trends, rather than platform-disclosed bidder counts.

Programmatic Auction Bid Depth Trend: Rising Seller Overcrowding in Tier 1 SEA Markets

This means more DSPs are chasing the same inventory, more advertisers are bidding on identical user segments, and more intermediaries are extracting margin from each transaction. What makes this phenomenon particularly damaging for Southeast Asia is the supply-side fragmentation. Unlike mature markets where inventory consolidation has already occurred, SEA's programmatic ecosystem remains fractured across hundreds of SSPs, regional exchanges, and walled gardens. There are now over 250 retail media networks (RMNs) globally, with Shopee, Lazada, Tokopedia, and TikTok Shop creating closed ecosystems that force advertisers into redundant platform relationships.

This fragmentation creates three specific problems:

More auction paths = Higher intermediary costs. Multiple SSPs, ad exchanges, and verification layers mean margin stacking. Even with first-price auctions becoming standard, buyers are often competing against themselves across different supply paths.

DSP proliferation. Southeast Asia alone saw 40+ new DSPs launched in 2024 focused on AI-based targeting. Each new DSP represents another bidder in the auction, driving up winning bids without corresponding increases in inventory quality.

Inefficient supply paths. Supply Path Optimization (SPO) remains nascent in SEA. Buyers working with curated private marketplaces pay 15-25% premiums to avoid the open auction chaos, but most mid-market advertisers still bid in open exchanges where CPM inflation is steepest.

The seller overcrowding effect is self-reinforcing: As CPMs rise, more advertisers and agencies optimize their SEA budgets, attracting more DSPs and platforms, which drives CPMs higher still. This cycle accelerates until either inventory quality improves dramatically or demand collapses.

Platform Concentration and First-Price Auctions: A Structural CPM Accelerator

One of the most underappreciated drivers of SEA CPM inflation is the simultaneous shift toward platform concentration and first-price auction mechanics.

Across social, commerce, and programmatic ecosystems in SEA, platforms have increasingly:

Consolidated demand within closed auction environments

Migrated inventory from second-price to first-price auctions

Reduced transparency across parallel supply paths

The effect is subtle but powerful.

Under first-price auctions, advertisers pay their true bid, not a marginal premium above the second-highest bidder. In markets where auction competition is rising as it is across Tier-1 SEA this mechanically lifts effective CPMs by 5–15% even when inventory quality remains unchanged.

At the same time, platform concentration amplifies pricing power:

Advertisers are increasingly forced to participate in a small number of “must-buy” environments

Demand collapses into fewer auctions

Competitive pressure intensifies without corresponding inventory expansion

This is not unique to any single platform; it is a structural shift in how digital advertising is priced in SEA.

Crucially, this dynamic is emerging before supply consolidation or data standardisation has matured, creating a period where costs rise faster than efficiency improves.

The Maturity Paradox: Why Cost ≠ Development

Here's the counterintuitive insight that separates sophisticated performance marketers from those caught in outdated frameworks: rising costs in SEA markets are not a sign of market maturity, they're a sign of chaotic supply dynamics in immature markets.

Mature markets like the US and UK have high CPMs because supply is deeply consolidated (a few dominant publishers control 70%+ of premium inventory), demand is efficient (sophisticated DSPs optimize across known supply paths), and inventory is scarce (marginal cost of additional impressions is high).

Southeast Asia has high CPMs for entirely different reasons: supply is fragmented across hundreds of platforms and walled gardens, demand is redundant (bidders chase identical inventory across multiple paths), and inventory is abundant but poorly organized (millions of impressions available but scattered across non-premium, non-viewable, and low-engagement environments).

This distinction matters because it suggests that SEA's cost inflation is temporary and unsustainable. As evidence, consider three key factors:

Retail Media consolidation is just beginning. Shopee, Lazada, and TikTok Shop operate parallel ad networks with limited interoperability. Unlike Amazon's dominance in the US retail ad market, no single player controls SEA's e-commerce advertising, forcing advertisers to buy across multiple fragmented platforms. Once consolidation occurs (likely 2025-2026), CPMs should stabilize or decline as arbitrage opportunities diminish.

Programmatic infrastructure maturity lags demand. Only 69.21% of SEA's out-of-home advertising was programmatic as of 2024; the remaining 30% relies on direct negotiation and legacy sales. This mixed ecosystem creates inefficiencies and margins that sophisticated buyers can arbitrage. Mature programmatic markets have near-100% programmatic adoption and lower intermediary costs.

First-party data strategy is still emerging. Retail media networks in SEA are only beginning to integrate first-party shopper data into programmatic auctions. Unlike mature markets where RMN buyers can confidently rely on probabilistic targeting without cookies, SEA advertisers are paying premiums for data enrichment and ID solutions that are still being standardized. As these standards solidify, CPMs should normalize downward.

The market is experiencing high costs not because it's mature, but because it's immature and chaotic competitive intensity without efficiency. Performance marketers treating SEA as a mature market (and paying mature-market CPM rates) are fundamentally mispricing their exposure.

What This Means for Performance Marketing Strategy in SEA

The data suggests performance marketers need to fundamentally rethink their SEA approach. Rather than treating CPM inflation as a market maturity signal and accepting higher costs, sophisticated teams should:

Implement aggressive Supply Path Optimization (SPO): Identify which SSPs and direct publisher relationships deliver the best CPM-to-conversion rates. In fragmented markets like SEA, SPO can reduce effective CPMs by 15-25% without sacrificing volume or quality. Focus on curated private marketplaces (PMPs) with Shopee, Lazada, and emerging players that offer premium inventory at lower intermediary costs than open exchanges.

Diversify away from TikTok's auctions: While TikTok is essential, excessive concentration on a single auction dynamic exposes you to CPM inflation driven by ByteDance's pricing power. Invest in emerging alternatives: retail media integration with Grab's advertising platform (which connects ride-hail users to in-store purchase paths), DOOH programmatic channels (growing 7.19% CAGR with less competitive pressure than digital), and search advertising on Tokopedia and Shopee (which command lower CPMs than TikTok but offer high-intent users).

Target audience composition with intention: Not all SEA consumers are equally competitive to reach. Tier 1 city audiences (Bangkok, Manila, Ho Chi Minh City, Jakarta) are driving 70%+ of CPM inflation due to advertiser concentration. Lower-tier audiences in secondary cities and provincial markets maintain CPMs 30-50% below Tier 1, often with comparable engagement rates.

Accelerate first-party data infrastructure: The RMNs and e-commerce platforms offering first-party shopper data access are the future of efficient SEA advertising. Building integrations with Shopee's advertising API, Grab's data partnerships, and TikTok Shop's advertiser tools today creates a competitive moat as identity solutions mature and reduce CPM inflation from data-enrichment premiums.

Hedge against consolidation: If Shopee and Lazada consolidate (both controlled by different parent companies, making consolidation unlikely but not impossible), or if a new player (likely ByteDance's TikTok Shop given its trajectory) dominates e-commerce advertising, CPMs will re-centralize and potentially decline. Diversifying across platforms now positions you to capture upside if consolidation winners emerge with efficiency gains.

Conclusion: SEA's Cost Inflation Is a Feature, Not a Bug And It's Temporary

Southeast Asia's rise as an expensive performance marketing region is neither a sign of success nor a permanent market condition. It's the result of immature supply dynamics, fragmented inventory, seller overcrowding, and a must-buy psychology around TikTok colliding with still-rising consumer spending power and e-commerce penetration.

Performance marketers who treat SEA's high CPMs as a signal to reduce or exit the region are making a strategic error. Conversely, those who accept high CPMs as a permanent cost of doing business in "mature emerging markets" are leaving value on the table through inefficient supply path management and platform concentration risk.

The real opportunity lies in recognizing that SEA's cost inflation is temporarily driven by supply chaos, not supply scarcity. By implementing disciplined supply path optimization, diversifying away from auction overcrowding, and building first-party data infrastructure, performance teams can maintain healthy unit economics and position for margin expansion as the market inevitably consolidates and standardizes over the next 18-24 months. The region's cost inflation paradoxically proves that Southeast Asia remains one of the highest-ROI markets for performance marketers willing to navigate its structural inefficiencies not despite them, but because of them.